SMM Alumina Morning Comment on May 19

Futures Market: Overnight, the most-traded alumina 2509 futures contract opened at 2,938 yuan/mt, with a high of 3,149 yuan/mt, a low of 2,921 yuan/mt, and closed at 3,141 yuan/mt, up 222 yuan/mt or 7.59%, with an open interest of 348,000 lots.

Ore: As of May 16, the SMM Import Bauxite Index stood at $70.41/mt, unchanged from the previous trading day. The SMM Guinea Bauxite CIF average price was $70/mt, unchanged from the previous trading day. The SMM Australia Low-Temperature Bauxite CIF average price was $70/mt, unchanged from the previous trading day. The SMM Australia High-Temperature Bauxite CIF average price was $65/mt, unchanged from the previous trading day.

Industry News:

- On May 14, the Guinean government ordered the revocation of industrial and semi-industrial mining licenses for over 40 mining companies, including "Axis Minérales, substance, Bauxite, Nature de l’acte d’octroi, D-2018-267-PRG SGG, Date d’octroi et de fin, 2-11-2018-1er-11-2033". It is understood that this mining right involves some projects that are currently mining and exporting bauxite. Recently, it was reported that the ongoing projects in this mining area received a notice of suspension, involving an annual bauxite production capacity exceeding 10 million mt. Relevant companies may negotiate with the government. The specific impact remains to be evaluated, and SMM will continue to follow up. This news has sparked market concerns about the supply of bauxite raw materials, leading to a sharp rise in alumina futures during the night session. As of the news release, the most-traded alumina futures contract once approached the daily price limit, with an increase in open interest of nearly 10,000 lots.

- Bauxite Port Inventory: According to SMM statistics on May 16, the total bauxite inventory at 9 domestic ports was 19.25 million mt, a decrease of 460,000 mt from the previous week.

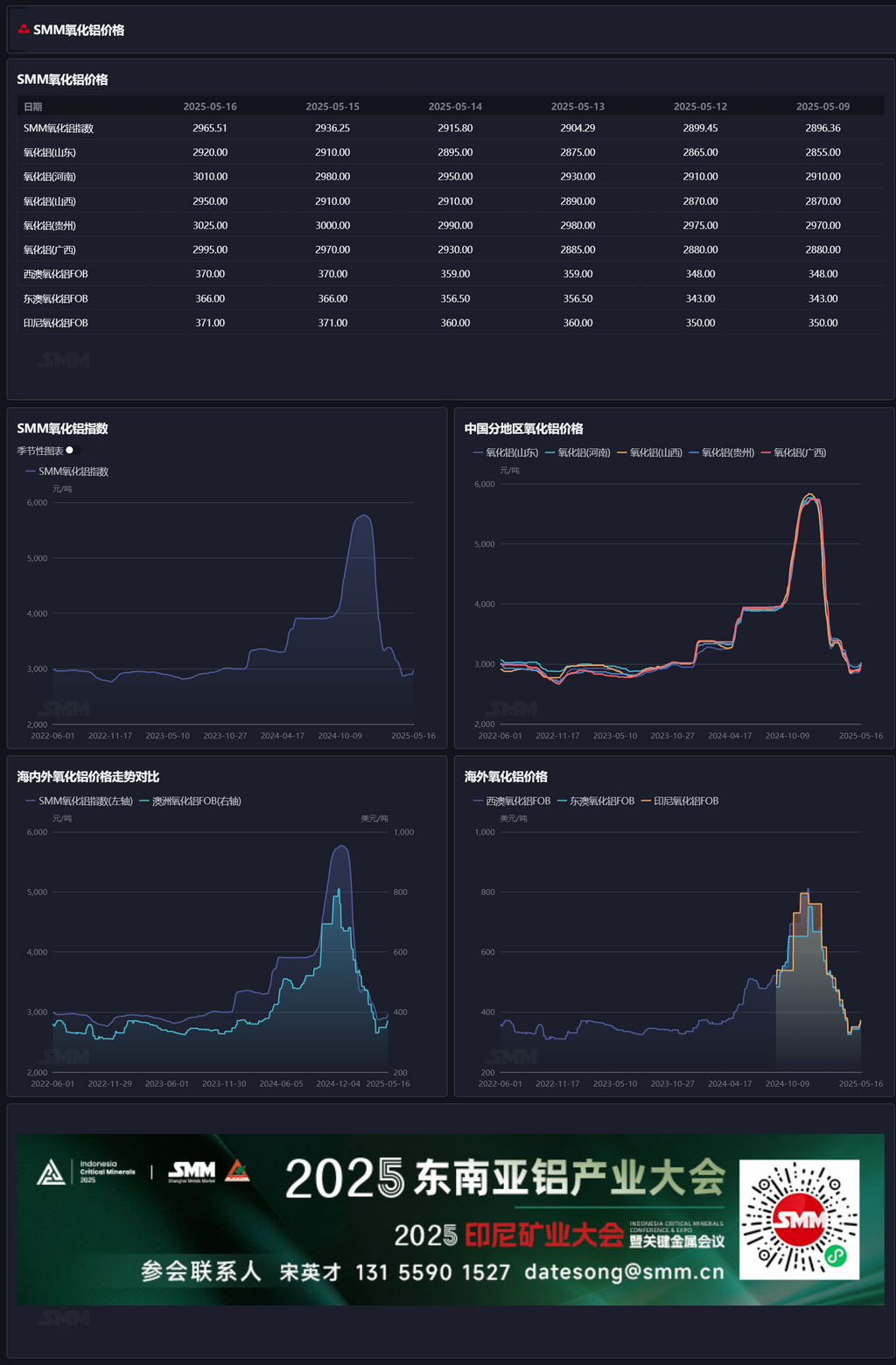

Spot-Futures Price Spread Daily Report: According to SMM data, on May 16, the SMM Alumina Index had a premium of 63.51 yuan/mt against the latest transaction price of the most-traded contract at 11:30.

Warrant Daily Report: On May 16, the total registered volume of alumina warrants decreased by 1,799 mt from the previous trading day to 197,500 mt. In the Shandong region, the total registered volume of alumina warrants remained unchanged at 601 mt from the previous trading day. In the Henan region, the total registered volume of alumina warrants remained unchanged at 3,001 mt from the previous trading day. In the Guangxi region, the total registered volume of alumina warrants decreased by 601 mt from the previous trading day to 12,600 mt. In the Gansu region, the total registered volume of alumina warrants remained unchanged at 6,306 mt from the previous trading day. In the Xinjiang region, the total registered volume of alumina warrants decreased by 1,198 mt from the previous trading day to 175,000 mt.

Overseas Market: As of May 16, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $21.50/mt. The USD/CNY exchange rate selling price was around 7.22. This price translates to an external selling price of approximately 3,274 yuan/mt at major domestic ports, which is 308 yuan/mt higher than the domestic alumina price. The alumina import window remained closed.

Summary: Last week, maintenance and production cuts were concentrated among alumina refineries in south China, with operating capacity decreasing by 2.9 million mt/year on a QoQ basis, leading to a further tightening of spot cargo availability. Additionally, alumina refineries have been facing losses in recent months, with a strong intention to refuse to budge on prices. Coupled with maintenance and production cuts, the tightening of spot cargo availability has led to a significant rebound in spot prices. In the futures market, during the night session last Friday, due to the revocation of mining rights for some enterprises in Guinea and the receipt of shutdown notices by some currently operating enterprises, involving significant capacity, concerns arose in the market regarding the supply of bauxite raw materials. This led to a sharp increase in futures prices, with the most-traded contract approaching the daily price limit, and the 2507 and 2508 contracts even hitting the daily price limit. It is reported that relevant enterprises are currently negotiating with the Guinean government, and the specific impact remains to be assessed. In the short term, this may provide sentiment-based support for bauxite prices, thereby offering cost support for alumina. Moving forward, it is necessary to continuously monitor changes in the operating capacity of alumina refineries, as well as the shipping volume of Guinean bauxite from the raw material side and the dynamics of relevant enterprises.